Introduction to Causal Inference: Double Machine Learning

Does a cash bonus shorten unemployment? Debiasing an RCT with ML

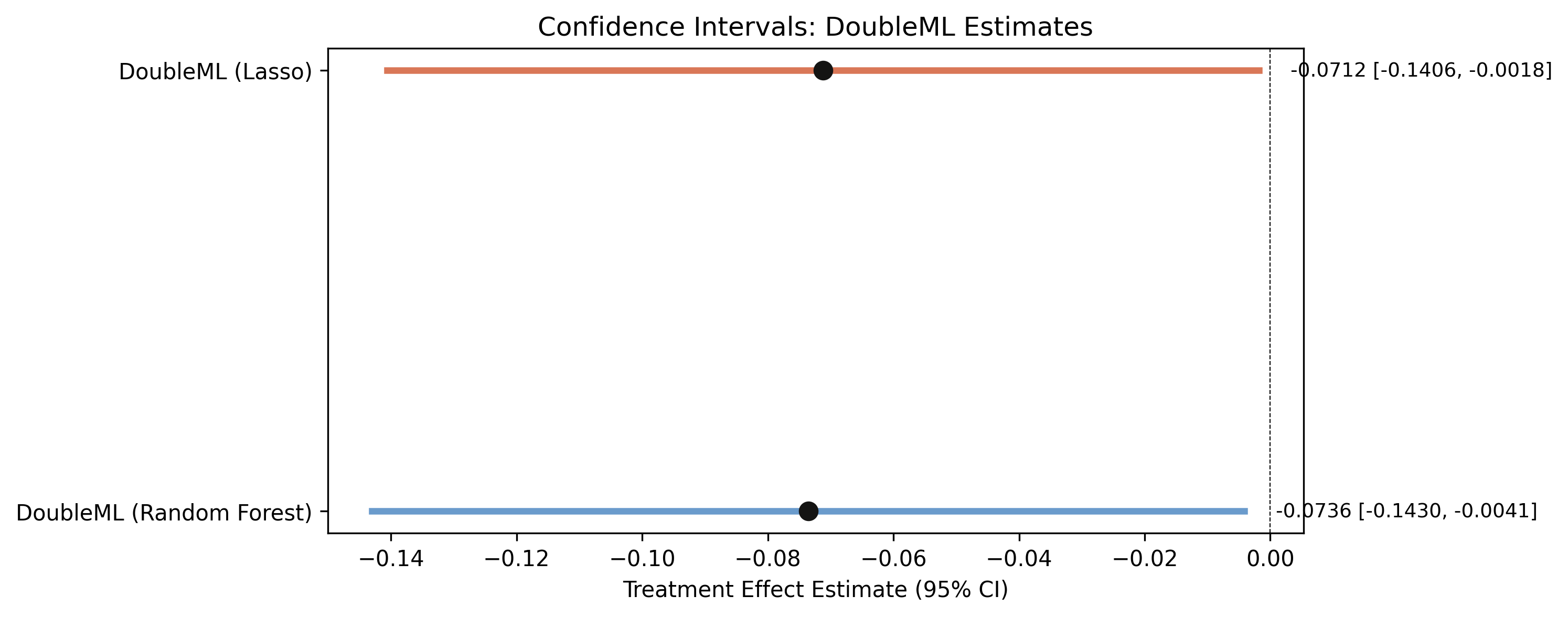

−0.0736DML · Random Forest

−0.0712DML · Lasso · same answer

5,099UI claimants · randomized

Nagoya University (GSID)

June 11, 2026

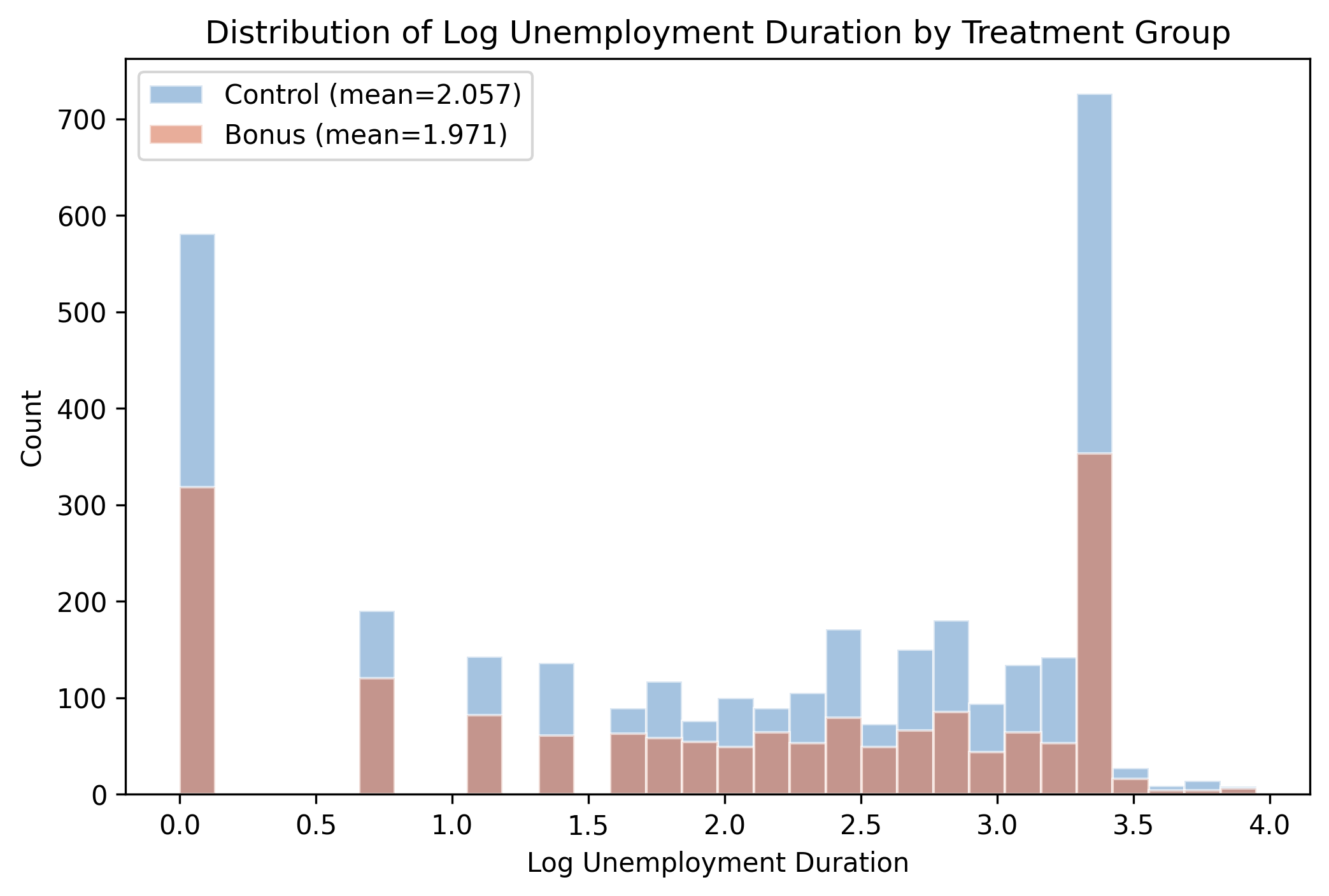

The raw gap is real but small: bonus duration sits ~0.09 log points lower

Log unemployment duration by group — both distributions pile up near 3.0–3.5; the bonus group’s mean sits ~0.09 log points lower.

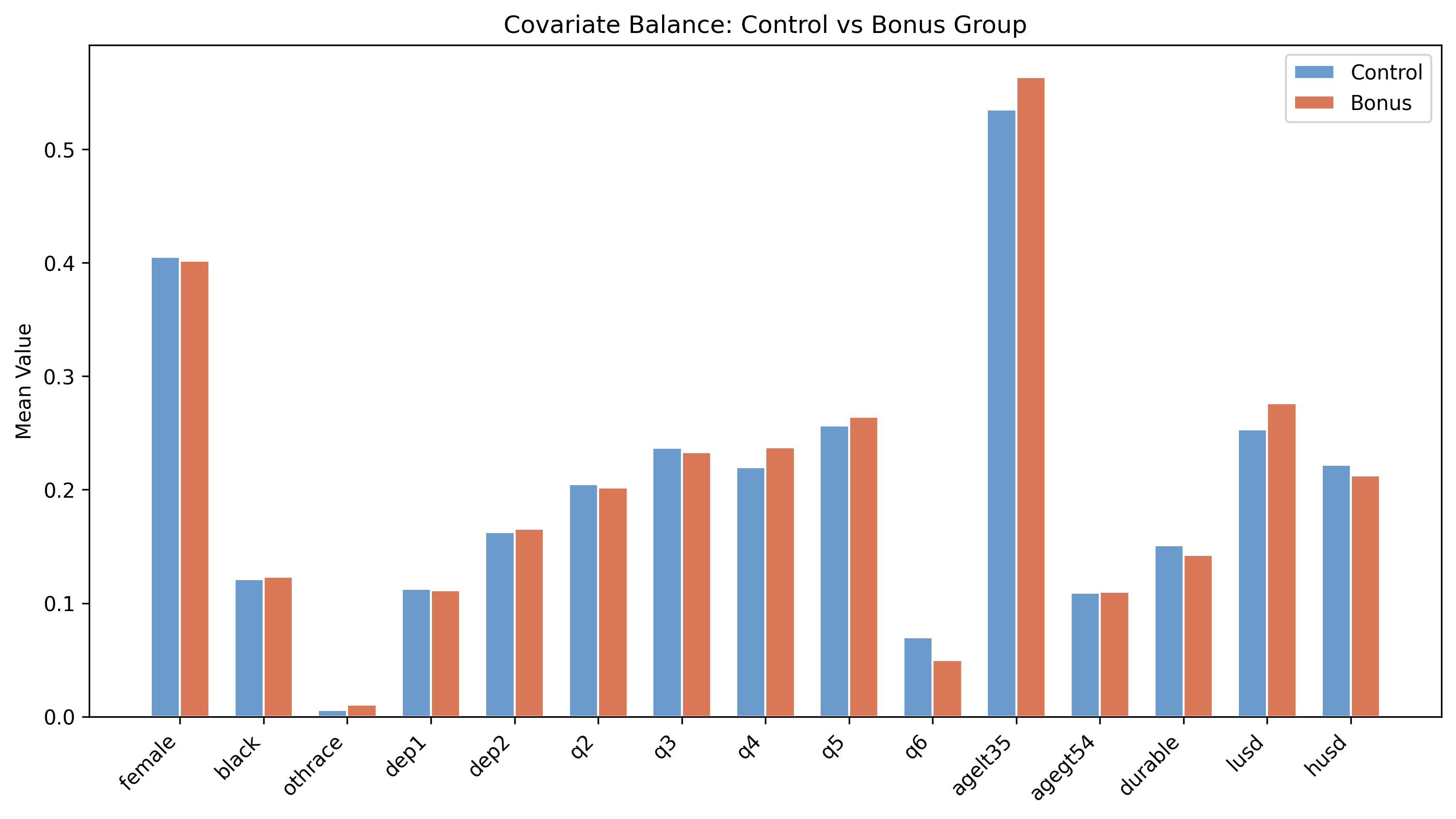

Randomization worked: covariate means line up almost exactly across groups

Mean of each of the 15 covariates, control (steel) vs bonus (orange) — the bars are nearly the same height everywhere.

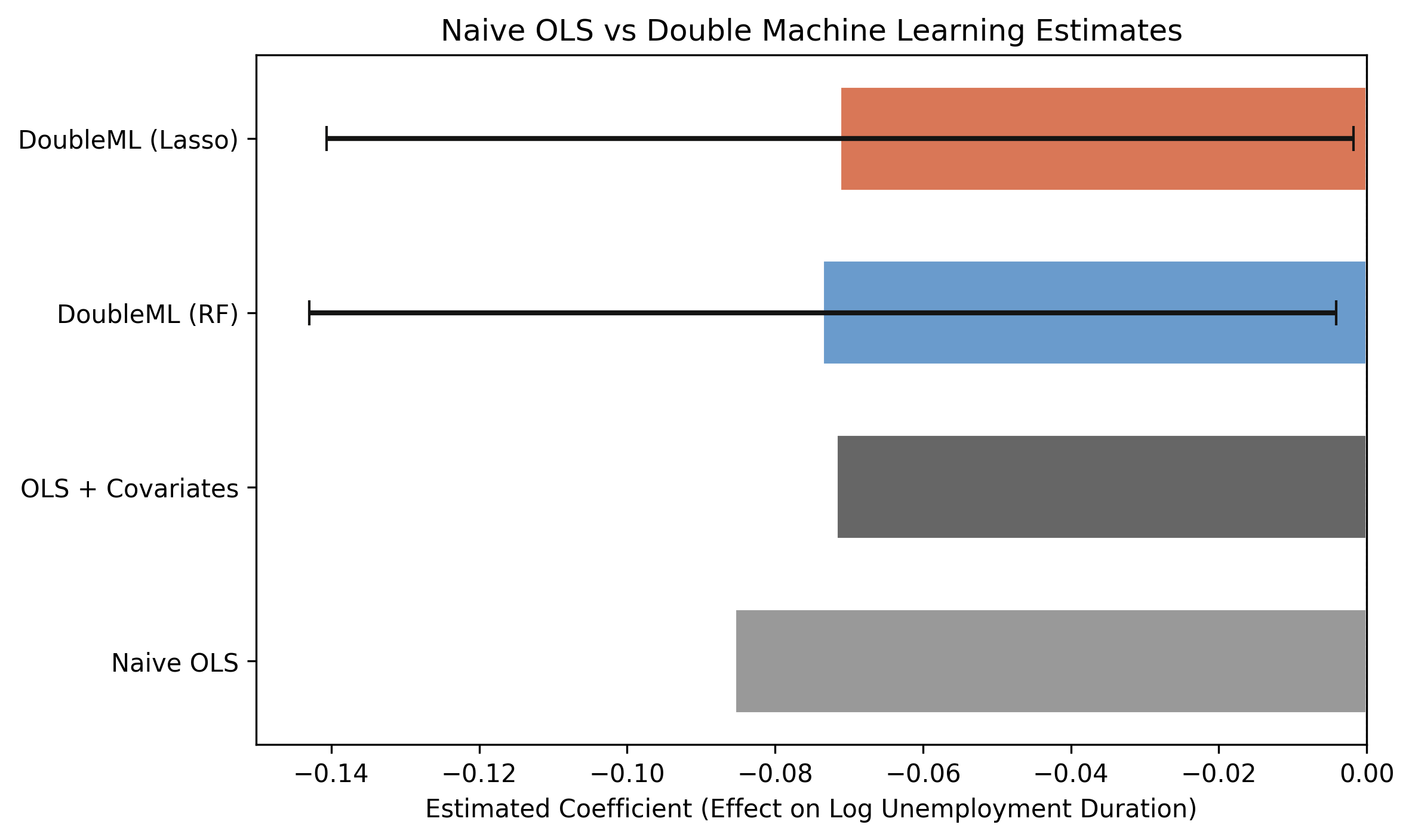

All four roads lead to ~−0.07: the methods agree on sign and size

Naive OLS (−0.0855) is largest; covariate OLS and both DML estimates cluster near −0.07. Dashed line = zero; only DML carries valid CIs.

Both DML intervals exclude zero — but only just

DML-RF [−0.143, −0.004] and DML-Lasso [−0.141, −0.002]; near-identical width, upper bounds hugging zero.