Same regression, same data — and shock half-lives of 1.5, 9, or 18 years

How much of this year’s employment shock is still visible next year?

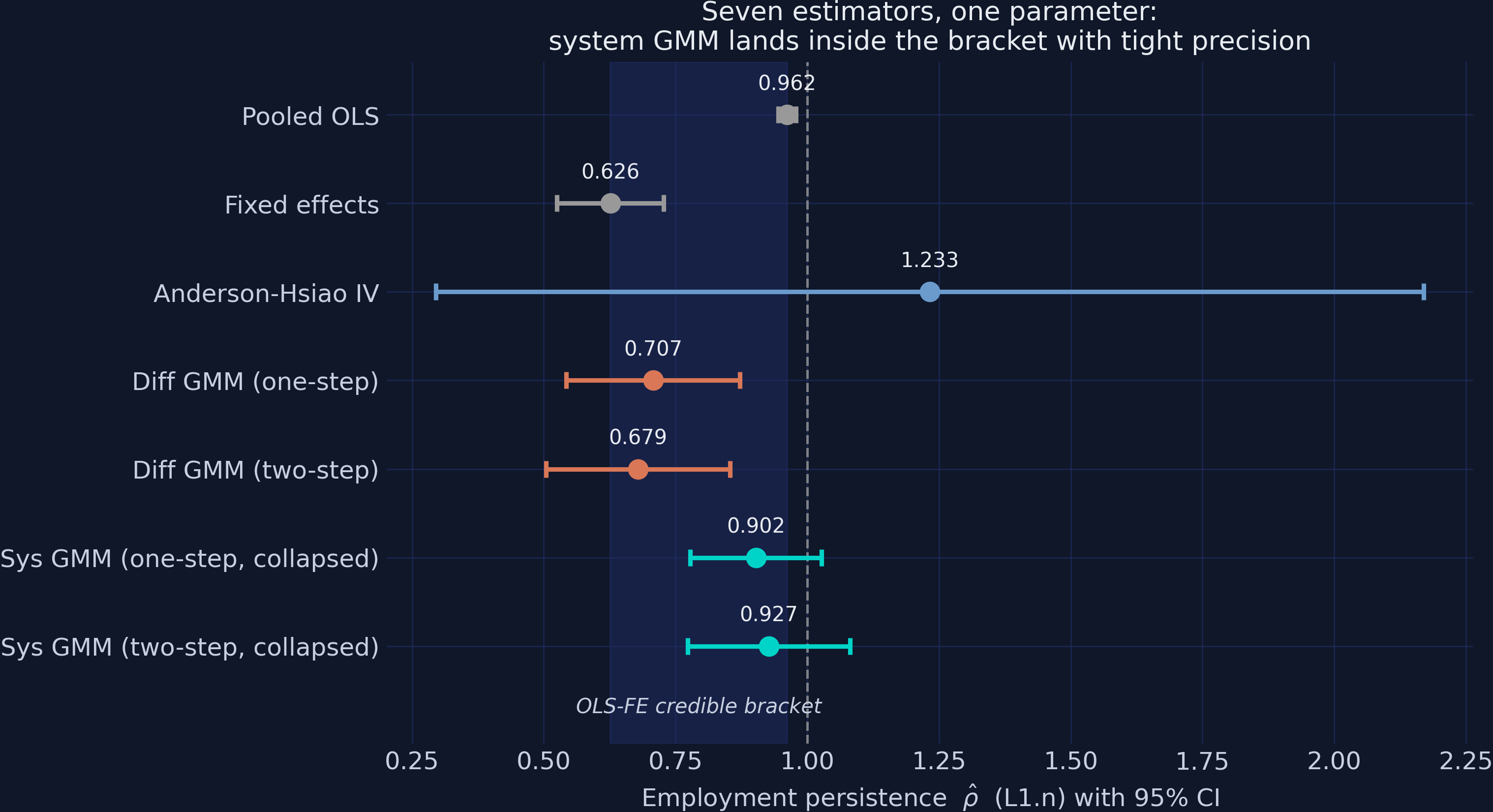

The answer is one number: \(\rho\), the coefficient on lagged employment. The estimators in this deck — run on the same 140-firm UK panel — will claim \(\hat\rho = 0.626\), \(0.927\), and \(0.962\).

One of them is defensible. None of them announces which.

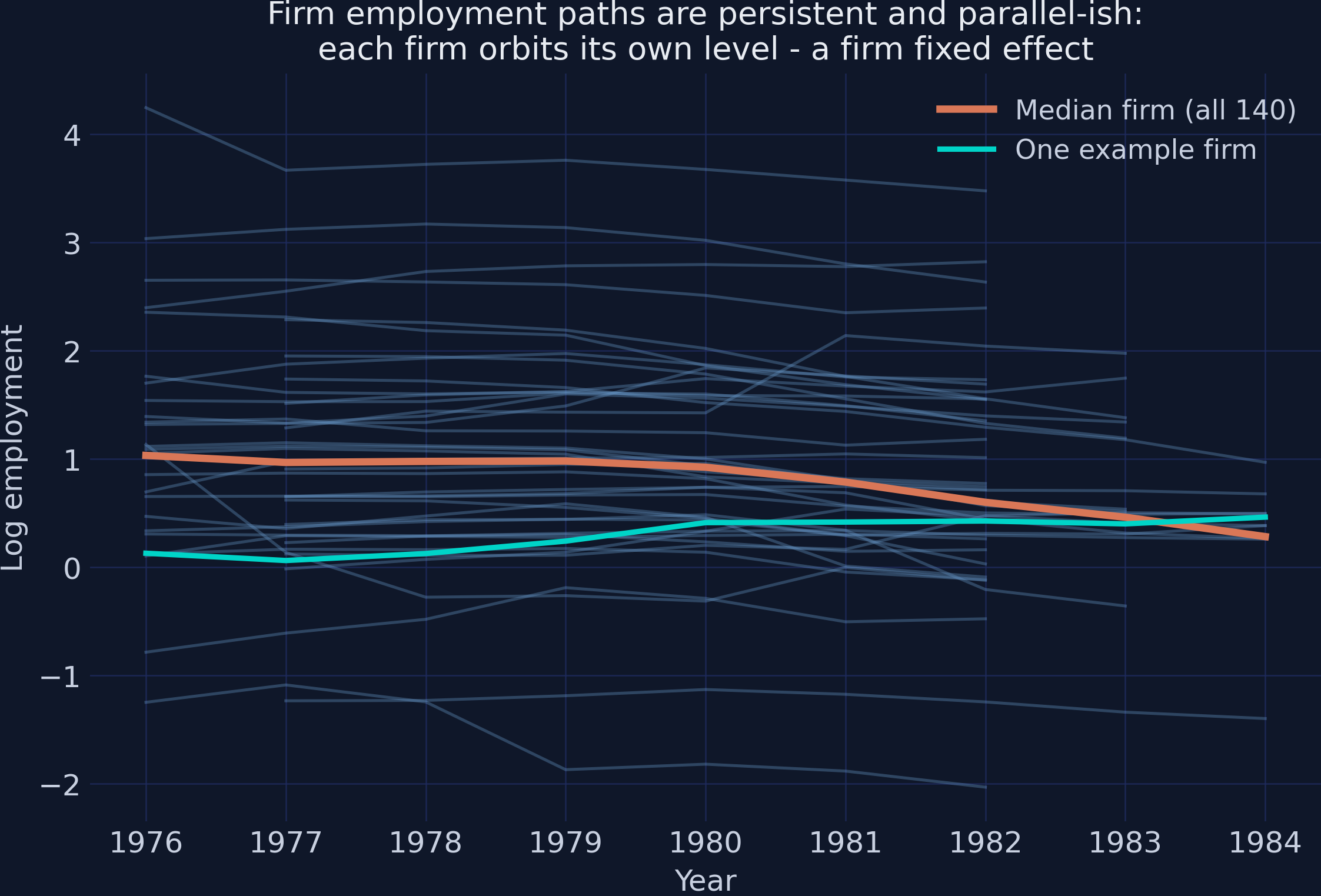

Firms orbit their own levels — a fixed effect and persistence at once

Each blue line is one firm, 1976–1984. Lines are parallel-ish (a firm fixed effect) and smooth (high persistence). The orange median dips after 1980 — the UK recession the year dummies absorb.

The model commits the one sin ordinary panel methods cannot forgive

A lagged dependent variable sits on the right while the firm effect \(\alpha_i\) sits in the error. By construction \(n_{i,t-1}\) depends on \(\alpha_i\) — so the regressor is correlated with the error, no matter how many controls we add.

Where we’re going

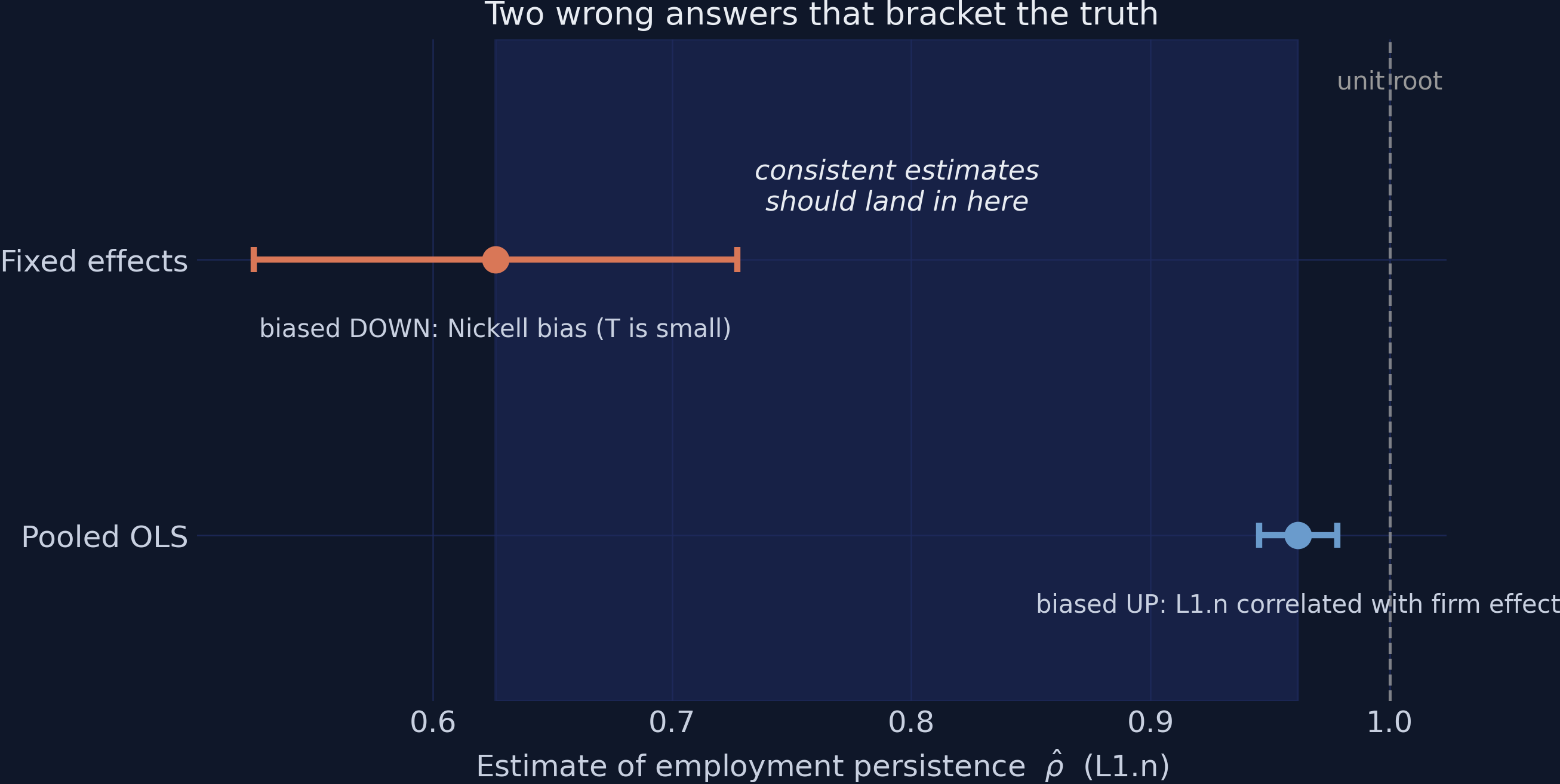

Run pooled OLS and fixed effects — two known-direction failures that bracket the truth

Anderson-Hsiao IV: consistent in theory, useless in practice

Difference GMM: passes every printed test, hugs the wrong bound

System GMM: the defensible headline, \(\hat\rho = 0.927\)

The diagnostics decoder — AR(1), AR(2), Hansen, and why p \(\approx\) 1 is a red flag

Instrument proliferation, collapsing, and a digit-for-digit replication check

The Investigation

Act II

Pooled OLS and fixed effects fail in opposite, known directions

Pooled OLS — biased UP

Ignores \(\alpha_i\): it stays in the error

\(n_{i,t-1}\) is positively correlated with \(\alpha_i\)

The lag gets credit for the firm effect’s work

\(\hat\rho = 0.962\) (SE 0.008) — near a unit root

Fixed effects — biased DOWN

Demeaning removes \(\alpha_i\) exactly…

…but the firm mean contains future shocks

Nickell bias, order \(1/T\) — and \(T\) is 7–9 here

\(\hat\rho = 0.626\) (SE 0.052)

Two wrong answers bracket the truth: any consistent estimate must land in [0.626, 0.962]

Bond’s (2002) bracket: OLS marks the ceiling, FE the floor. The shaded band is the playing field for every estimator that follows.

Anderson-Hsiao IV is consistent — and useless: 1.233 with a CI 1.87 wide

First-difference away \(\alpha_i\), then instrument \(\Delta n_{i,t-1}\) with the level \(n_{i,t-2}\):

Estimate

SE

95% CI

\(\hat\rho\) (Anderson-Hsiao 2SLS)

1.233

0.478

[0.296, 2.170]

The CI contains the whole bracket, the unit root, and explosive dynamics — all at once.

Arellano-Bond: every lag dated \(t-2\) or earlier is a valid instrument

\[E\big[\,n_{i,t-s}\,\Delta\varepsilon_{it}\,\big] = 0 \qquad \text{for all } s \ge 2\]

Employment two or more years ago carries no information about this year’s change in shocks — and the same holds for lagged \(w\) and \(k\). Dozens of moment conditions, combined optimally by GMM.

Two command strings run the whole GMM ladder in pydynpd

Even for a persistent series, last year’s change is informative about this year’s level. The price is one new assumption — mean stationarity: firms’ initial deviations from their steady states must be unrelated to \(\alpha_i\).

Ninety-three percent of an employment shock survives into next year

0.927

system GMM, two-step, 32 collapsed instruments (SE 0.079) — inside the bracket, upper half

The headline’s diagnostics are textbook-clean

Two-step system GMM (collapsed)

\(\hat\rho\) (L1.n)

0.927

SE (Windmeijer)

0.079

Instruments

32 (vs 140 firms)

AR(1) p

0.000 — rejects, as required

AR(2) p

0.994 — clean

Hansen p

0.462 — comfortable middle

Trust, But Verify

Act III

The diagnostics decoder: two of the three tests are read backwards

Test

Correct reading

Headline value

AR(1) in differences

Must reject — rejection is mechanical good news

p = 0.000 ✓

AR(2) in differences

Must not reject — this validates the \(t-2\) instruments

p = 0.994

Hansen J

Two-tailed in spirit — p < 0.05 is invalid; p near 1 is an overwhelmed test

p = 0.462 ✓

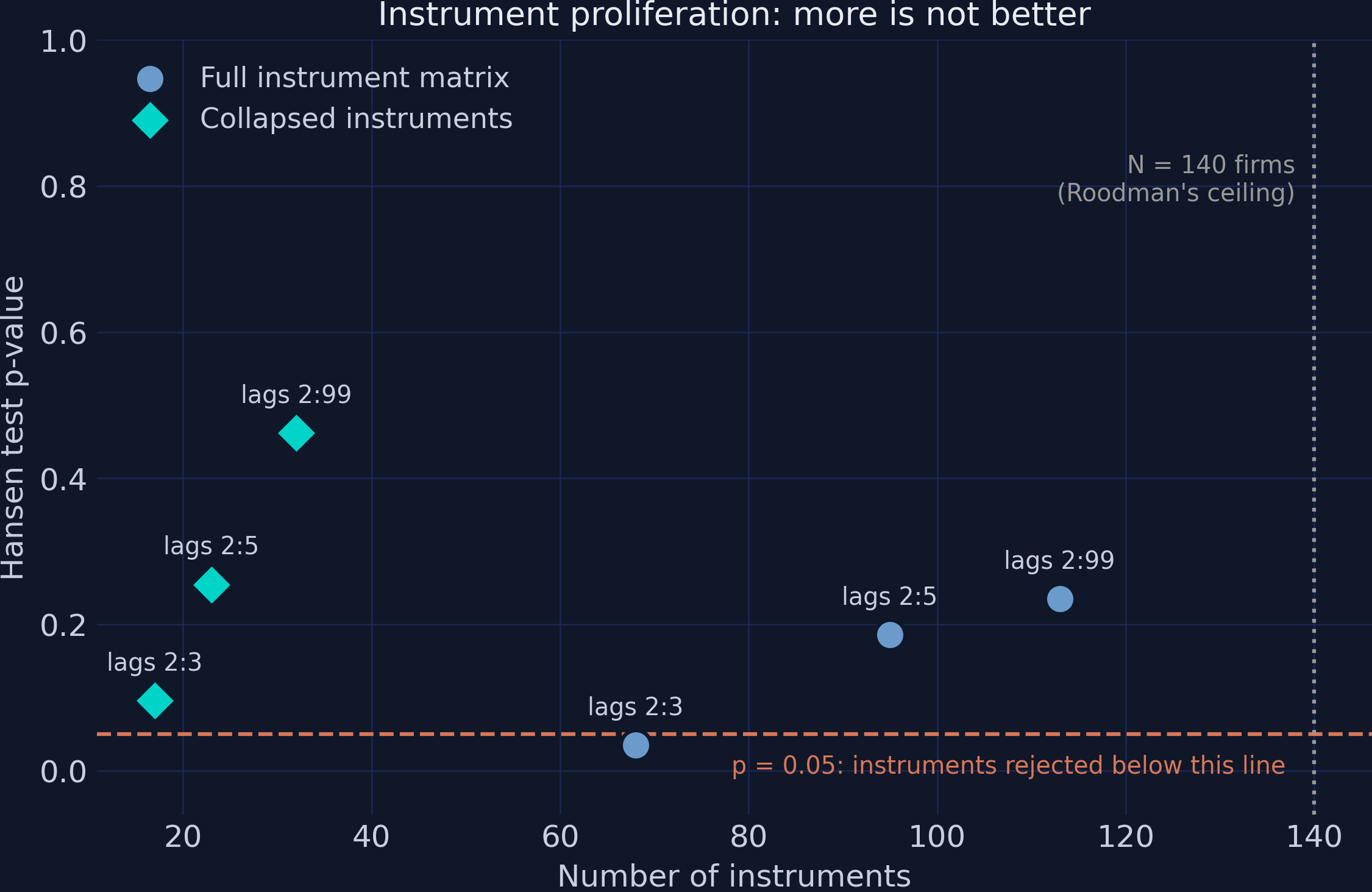

The Hansen p-value responds to the instrument count, not just validity

Lag window

Collapsed

Instruments

\(\hat\rho\)

Hansen p

2:3

no

68

0.956

0.035

2:3

yes

17

0.921

0.096

2:5

no

95

0.935

0.186

2:99

no

113

0.930

0.235

2:99

yes

32

0.927

0.462

Same model six times; only the plumbing changes. Uncollapsed 2:3 is rejected (p = 0.035) while its collapsed twin passes — driven purely by instrument count.

More instruments is not better — proliferation disarms the test that guards you

Hansen p against instrument count: full matrix (steel) vs collapsed (teal), the p = 0.05 rejection line, and the 140-firm Roodman ceiling.

The toolchain replicates the published benchmark digit for digit

Published vignette

Our run

L1.n

0.2710675

0.2710675

Hansen \(\chi^2\)

32.666

32.666

Instruments

42

42

Exact match under a hard assertion — the NumPy-2 compatibility shim perturbs nothing.

Seven estimators, one parameter — only the workflow identifies the winner

Every estimator with its 95% CI against the shaded OLS–FE bracket. Grey defines the band; blue (Anderson-Hsiao) straddles everything; orange (difference GMM) hugs the floor; teal (system GMM) lands in the upper half.

“Your own CI includes the unit root — why believe 0.927?”

Objection. The headline CI [0.773, 1.081] contains \(\rho = 1\), mean stationarity is untestable, and one common \(\rho\) is imposed on all 140 firms.

Response. All true — which is why the claim is the point estimate and its lower bound, never “employment is stationary.” The estimate survives the bracket check, a 6-cell proliferation grid (range 0.921–0.956), clean AR(2)/Hansen, and an exact replication — and the mean-stationarity price is stated out loud, not hidden.

The dynamic-panel checklist you take home

Run OLS and FE first — record the bracket; they are the measuring stick

A difference-GMM estimate hugging the FE bound is a weak-instrument symptom — passing Hansen and AR(2) does not clear it

Prefer system GMM when persistence is high — and name the mean-stationarity assumption you are buying

AR(1) must reject; AR(2) must not; read Hansen two-tailed

Collapse instruments and report the count relative to the number of groups

Replicate a published benchmark before trusting novel numbers

No single p-value separates 0.927 from 0.679 — the bracket-plus-diagnostics workflow does.