where \(\tilde x_1\) is the residual of \(x_1\) (coupons) regressed on \(x_2\) (income), and \(\tilde y\) is the residual of \(y\) (sales) regressed on \(x_2\).

Remove income from coupons, remove income from sales, then regress the leftovers. Same \(\hat\beta_1\).

Three lines of statsmodels reproduce the multivariate coefficient

# residualize each variable with respect to incomedf["coupons_tilde"] = smf.ols("coupons ~ income", df).fit().residdf["sales_tilde"] = smf.ols("sales ~ income", df).fit().resid# regress residual sales on residual coupons (no intercept)fwl = smf.ols("sales_tilde ~ coupons_tilde - 1", df).fit()

Residuals are mean-zero, so we drop the intercept. The coefficient on coupons_tildeis the controlled effect.

Residualize-both reproduces +0.2673 exactly — and recovers the SE

FWL step

Coupons coef.

SE

p

Step 1 — residualize \(x_1\) only

+0.2673

1.271

0.834

Step 2 — residualize both

+0.2673

0.118

0.028

Same coefficient to four decimals; residualizing the outcome too restores the SE to match full OLS (0.120).

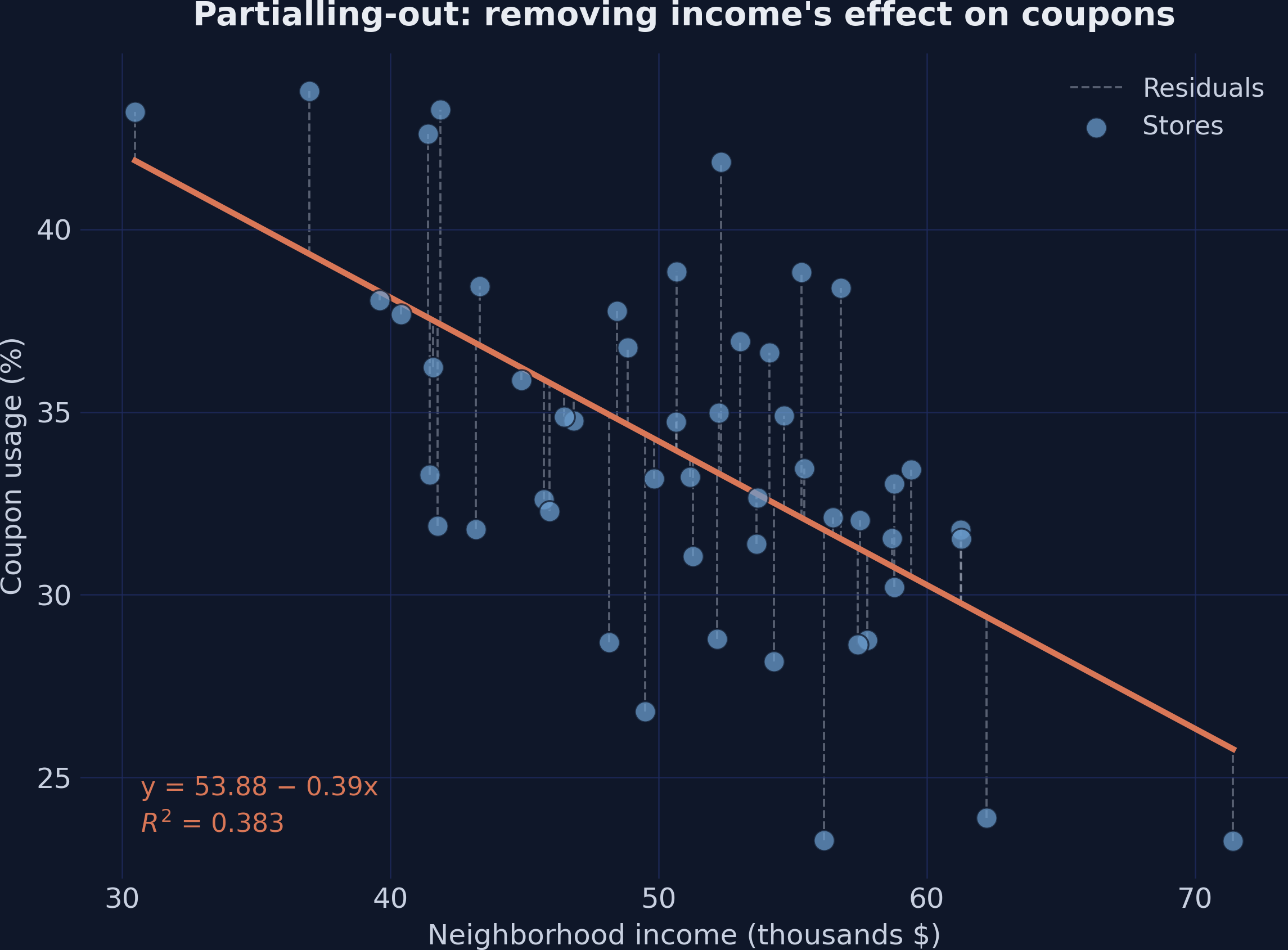

Partialling-out, drawn: the residuals are coupon variation income can’t explain

Coupon usage vs. income; the orange line is the income→coupons fit, dashed lines are the residuals each store keeps.

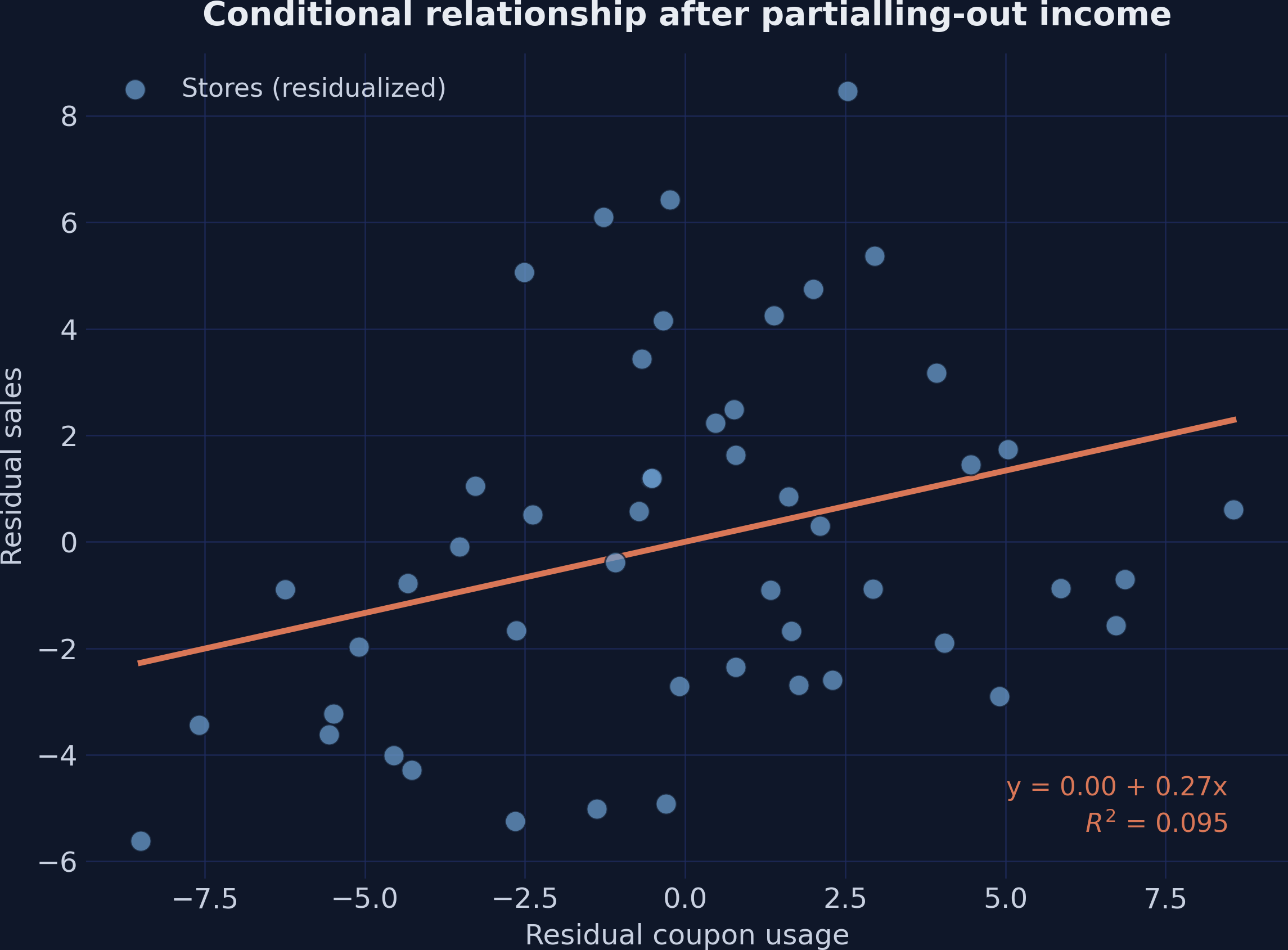

The hidden positive relationship the table couldn’t show you

Residualized sales vs. residualized coupons. With income removed from both, the slope is the +0.267 conditional effect.

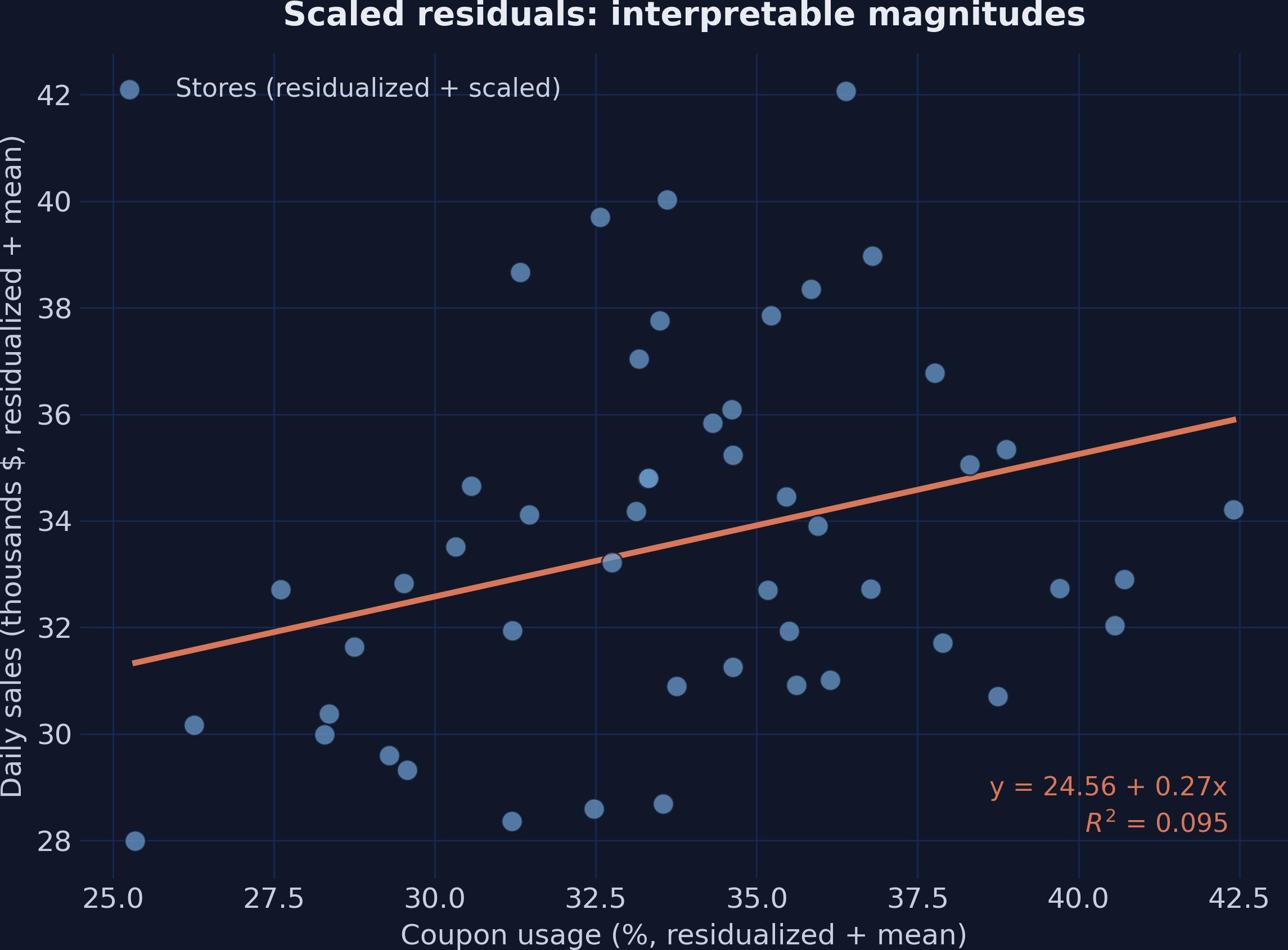

Adding the means back keeps the slope but restores readable units

Same residual scatter shifted by the sample means — axes now read ~34% coupons and ~$33.6K sales, slope still +0.267.

FWL scales: two controls, same identity, +0.2706

Model

Coupons coef.

SE

p

Full OLS (+ income + day)

+0.2706

0.119

0.028

FWL (+ income + day)

+0.2706

0.116

0.023

Partial out income and day-of-week from both sides — identical coefficient. The theorem holds for any number of controls.

The Resolution

Act III

After partialling-out income, coupons raise sales by +0.267

+0.267

\(\hat\beta_1\) on coupons, full OLS = FWL (SE 0.118) · matches the true +0.200 within finite-sample noise

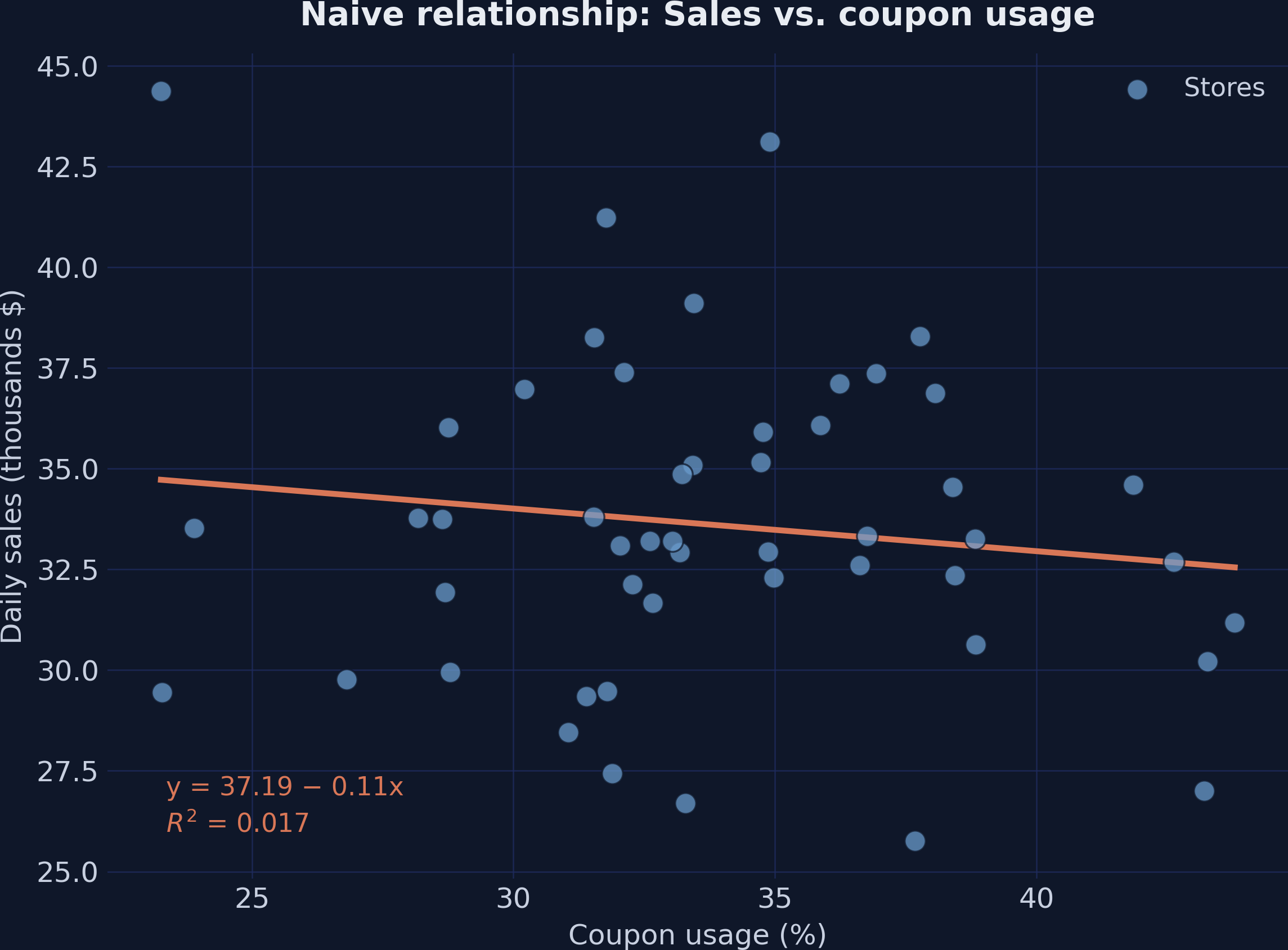

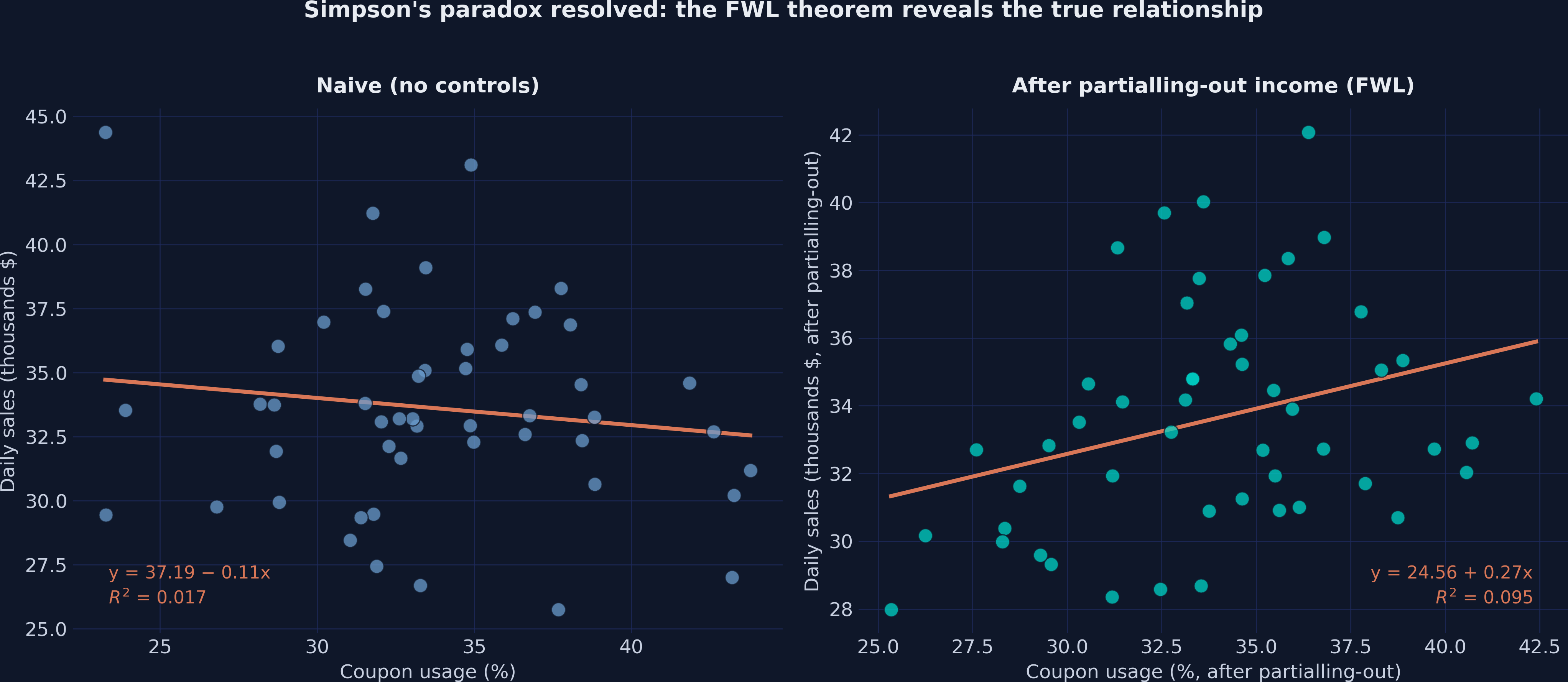

Simpson’s paradox, resolved: the slope flips from −0.106 to +0.267

Left: naive negative slope. Right: positive slope after partialling-out income. Same 50 stores.

Six estimators, one coefficient: FWL is an identity, not an approximation

Method

Coupons coef.

SE

p

Naive OLS (no controls)

−0.1059

0.116

0.365

Full OLS (+ income)

+0.2673

0.120

0.031

FWL residualize \(x\) only

+0.2673

1.271

0.834

FWL residualize both

+0.2673

0.118

0.028

Full OLS (+ income + day)

+0.2706

0.119

0.028

FWL (+ income + day)

+0.2706

0.116

0.023

Does FWL make this causal? No — it visualizes, it does not identify

Objection. Residualizing on income looks like a trick that manufactures a causal effect.

Response. FWL is pure algebra — it only reproduces what OLS already computes. The causal reading needs one assumption: income is the only confounder. FWL pictures that adjustment; it cannot certify it.

FWL is Double Machine Learning with a linear mop

FWL (here)

residualize \(y\), \(d\) with OLS

regress residual \(y\) on residual \(d\)

exact for linear confounding

Double ML

residualize \(y\), \(d\) with ML (forest, lasso)

regress residual \(y\) on residual \(d\)

handles non-linear, high-dim controls

Same residualize-then-regress logic; swap OLS for a flexible learner and you get a debiased causal estimate.

Don’t read the coefficient — read the partialled-out scatter.