Beta and Sigma Convergence Across Countries

Are poor countries catching up? A convergence toolkit in Stata

Nagoya University (GSID)

June 11, 2026

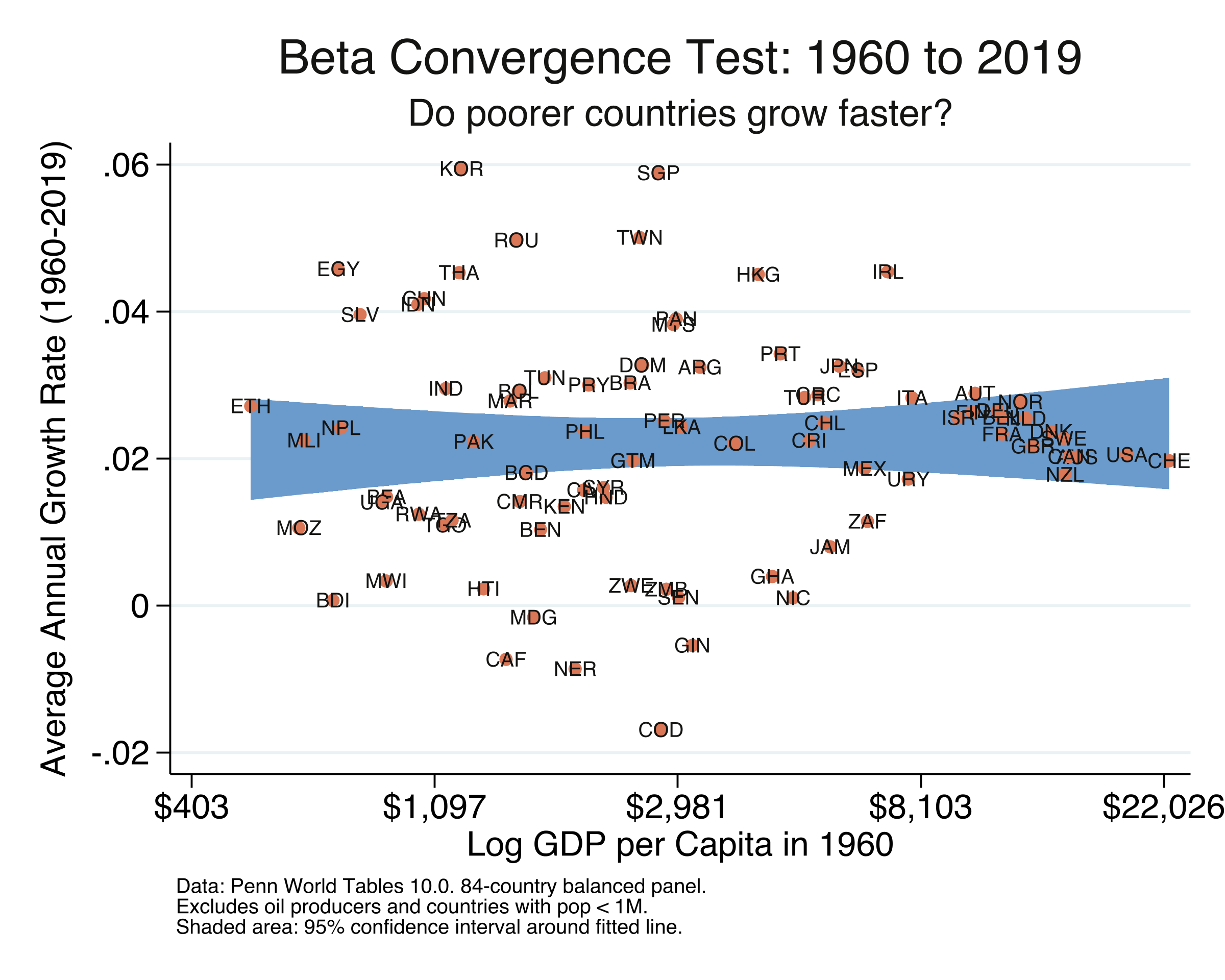

Over six decades, where a country started told you nothing about how fast it grew

Annualized growth (1960–2019) versus log initial income. The fitted line is flat: starting income has essentially no predictive power.

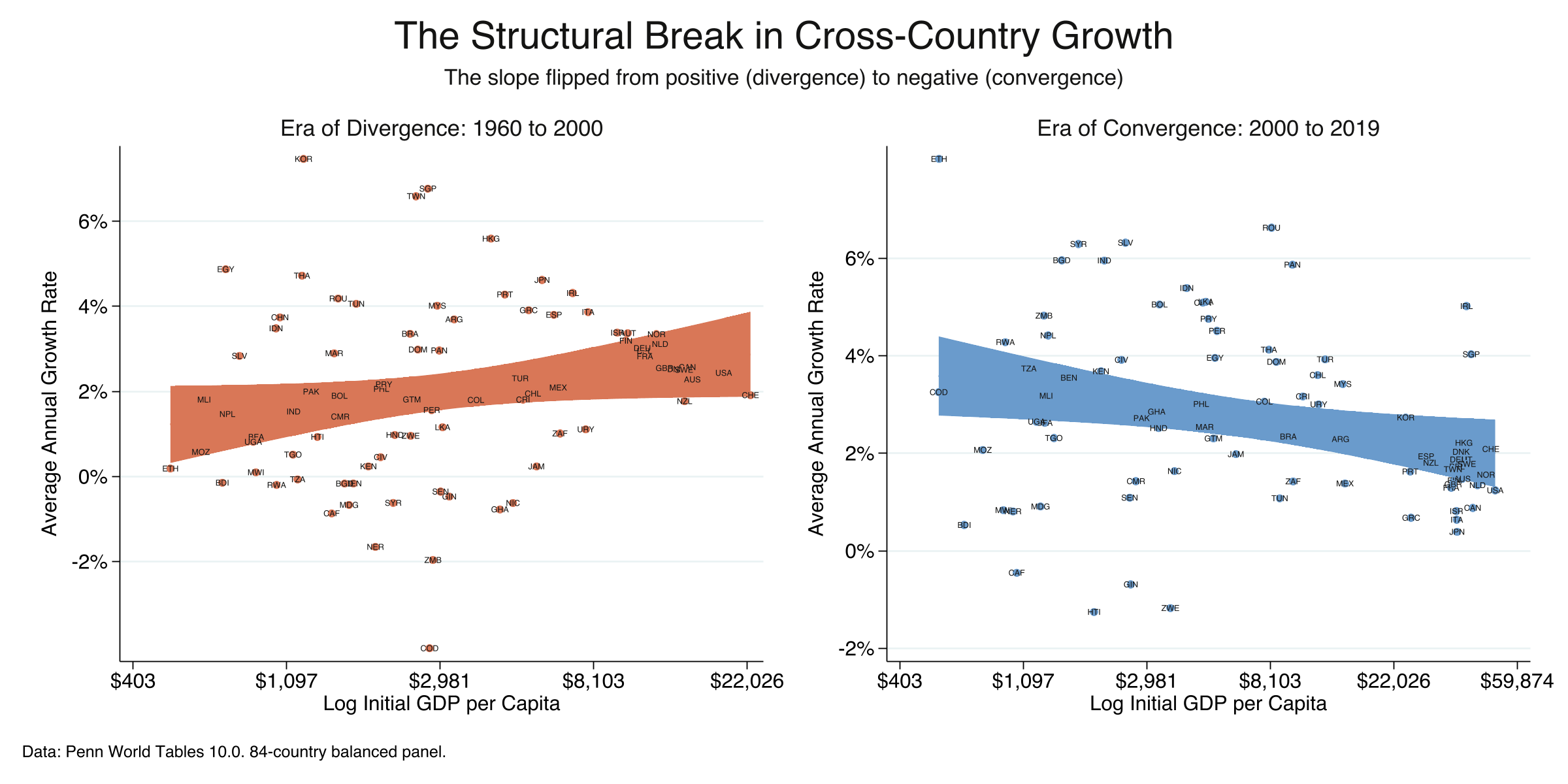

Split at 2000 and the flat line shatters into two opposite eras

Era of divergence (1960–2000, orange) versus era of convergence (2000–2019, steel): the slope flips sign.

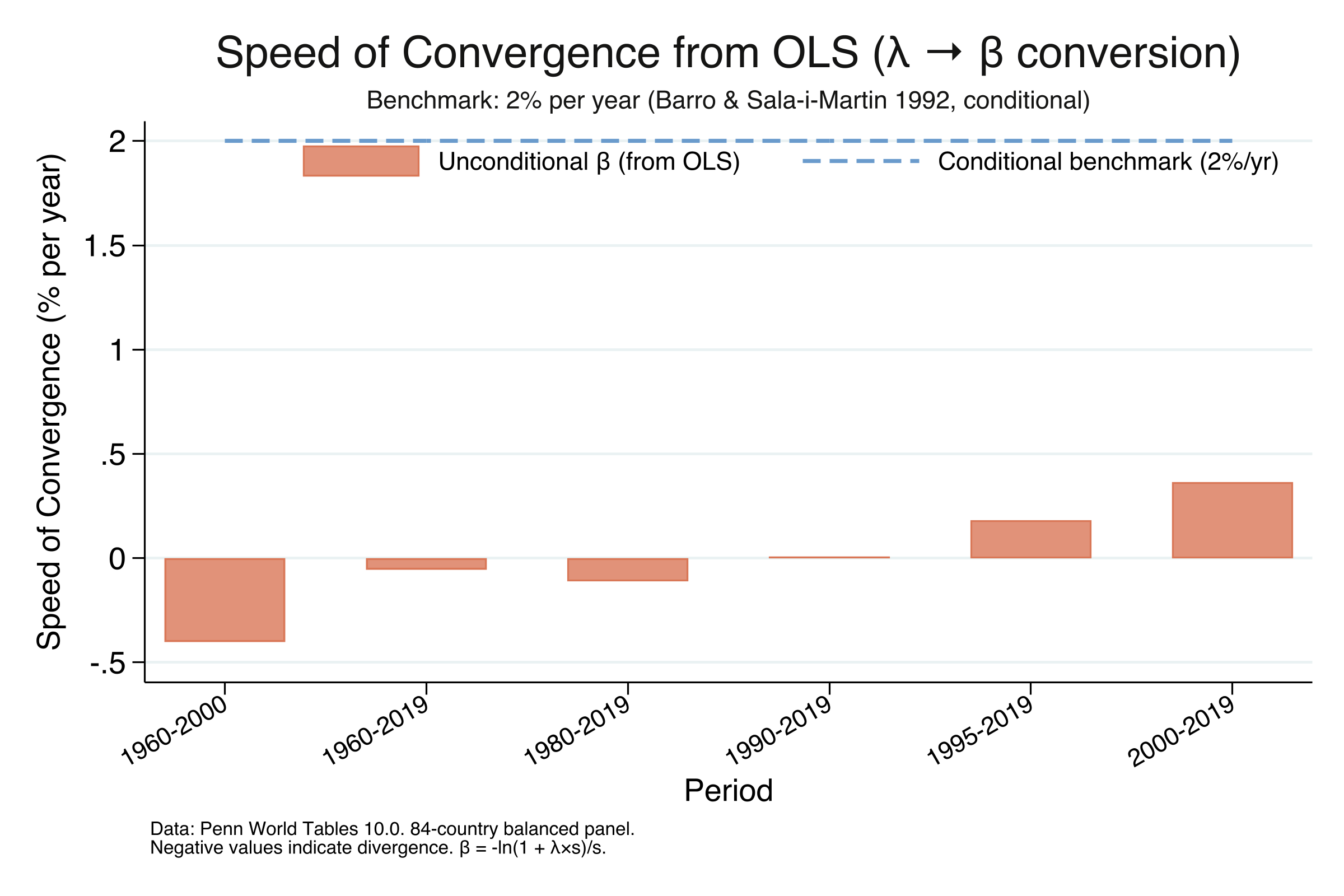

Convergence since 2000 runs at 0.36% a year — five times slower than the benchmark

Speed of unconditional convergence (β) across six windows; dashed line = the classic 2% conditional benchmark.

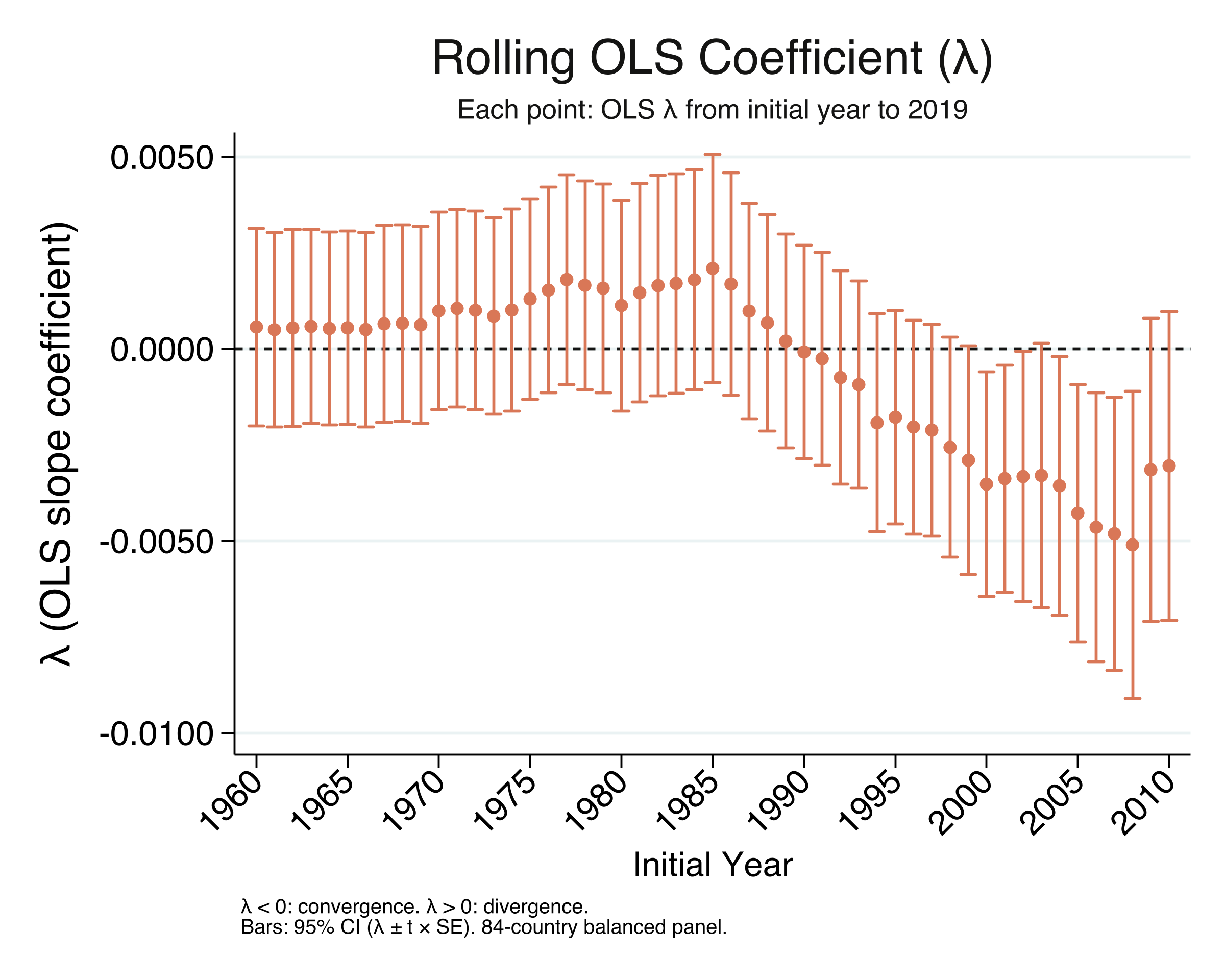

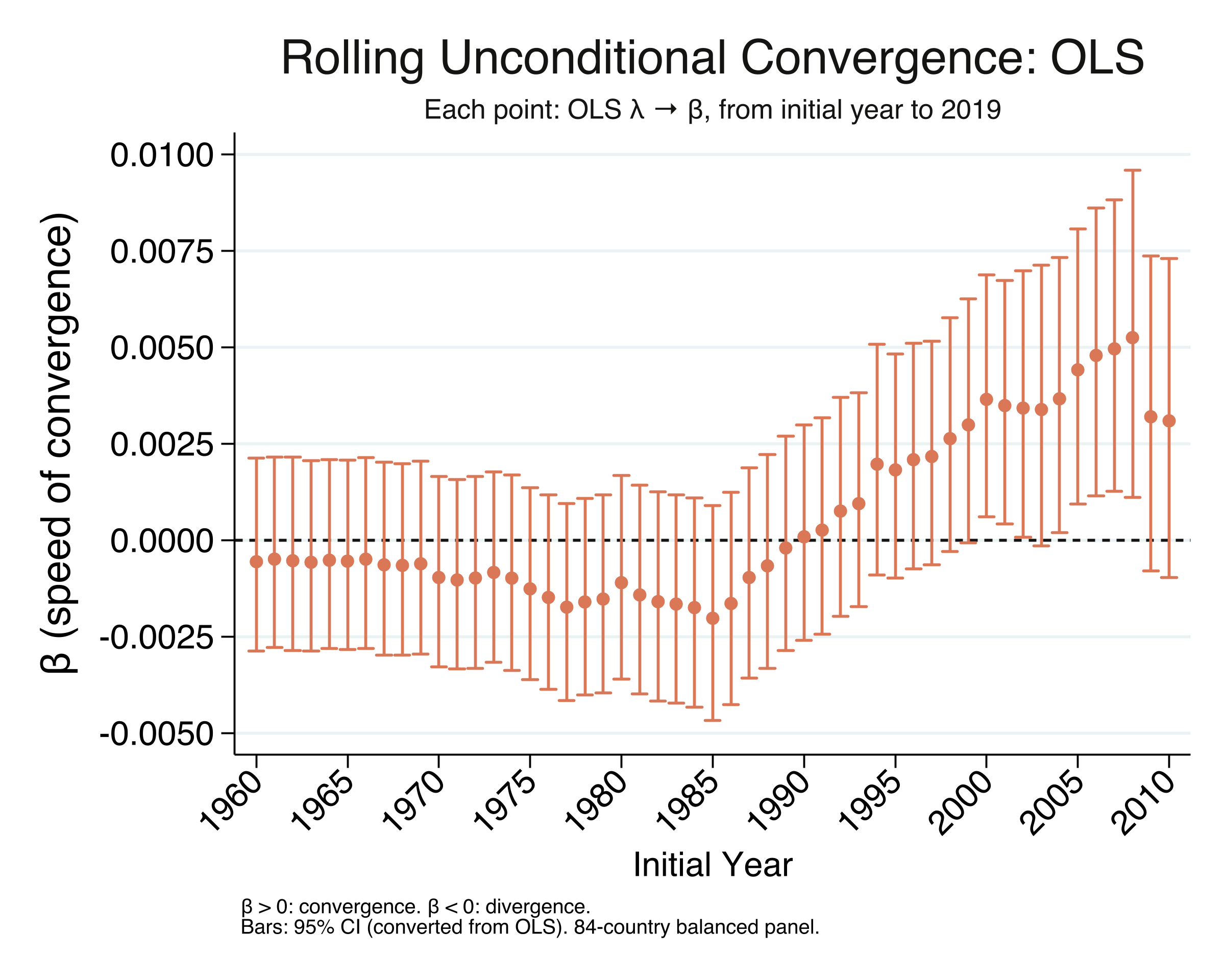

Watch convergence switch on: the rolling slope crosses zero around 1990

Rolling OLS \(\lambda\) from each start year to 2019, with 95% confidence intervals. Negative \(\lambda\) = convergence.

As \(\beta\), the same story peaks near 2005 then eases — the crisis footprint

Rolling structural \(\beta\) (OLS conversion; NLS is identical) from each start year to 2019, with 95% CIs.

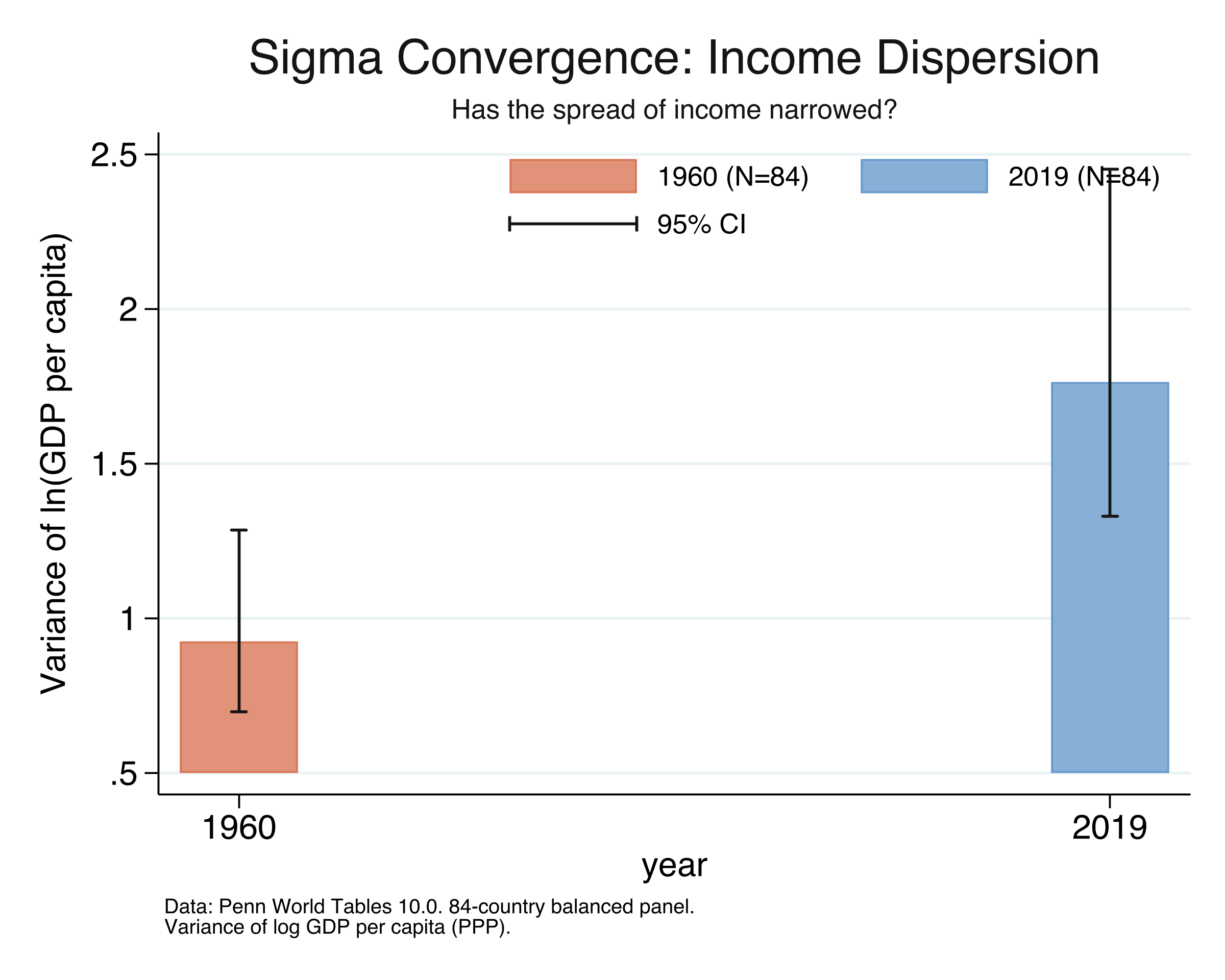

Beta convergence is real — yet the income spread grew by 91%

Variance of log GDP per capita, 1960 versus 2019 (same 84 countries), with chi-squared 95% CIs.

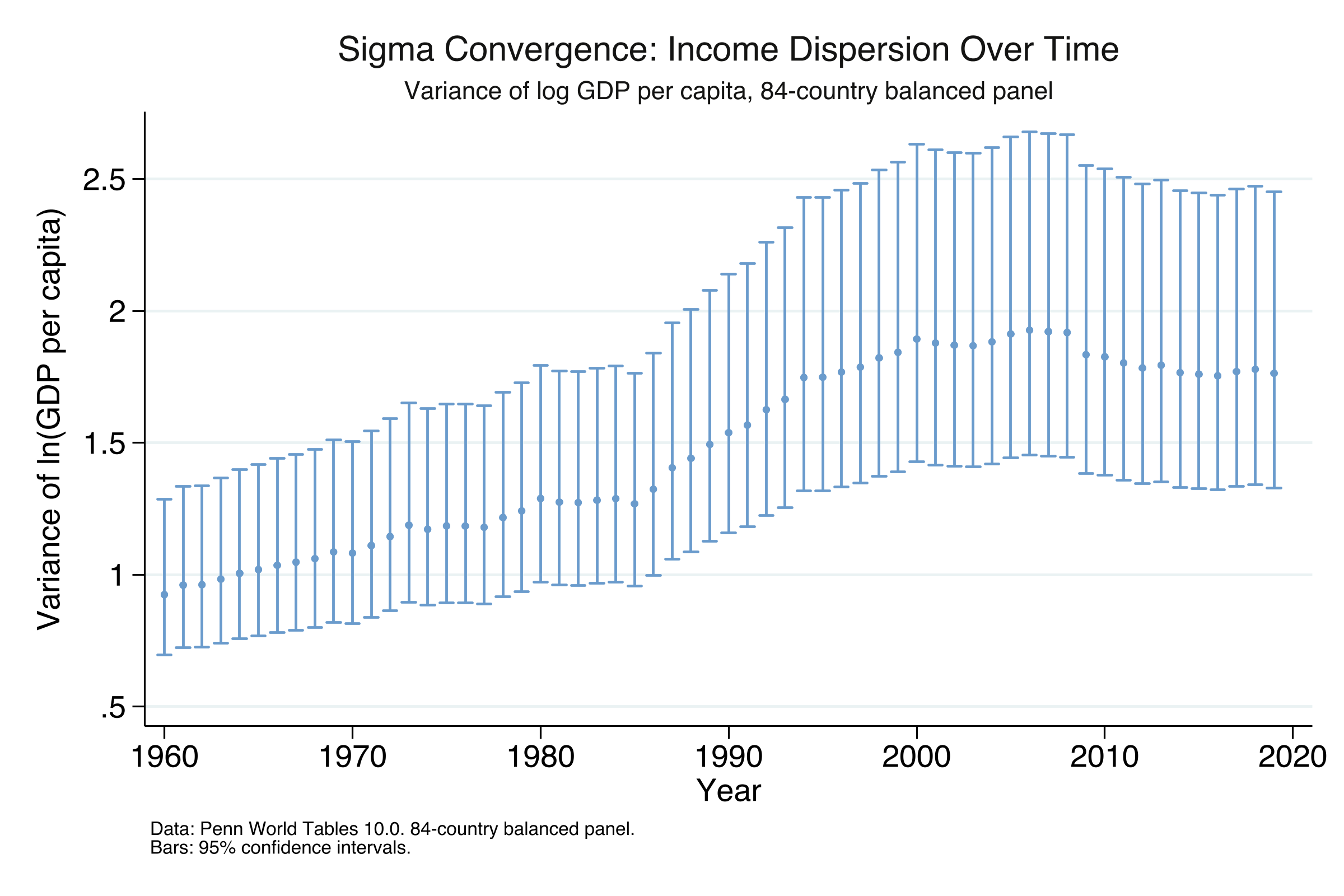

Sigma followed beta with an 8-year lag — and only after 2008

Year-by-year variance of log income (84-country panel). It peaks in 2008, then declines.

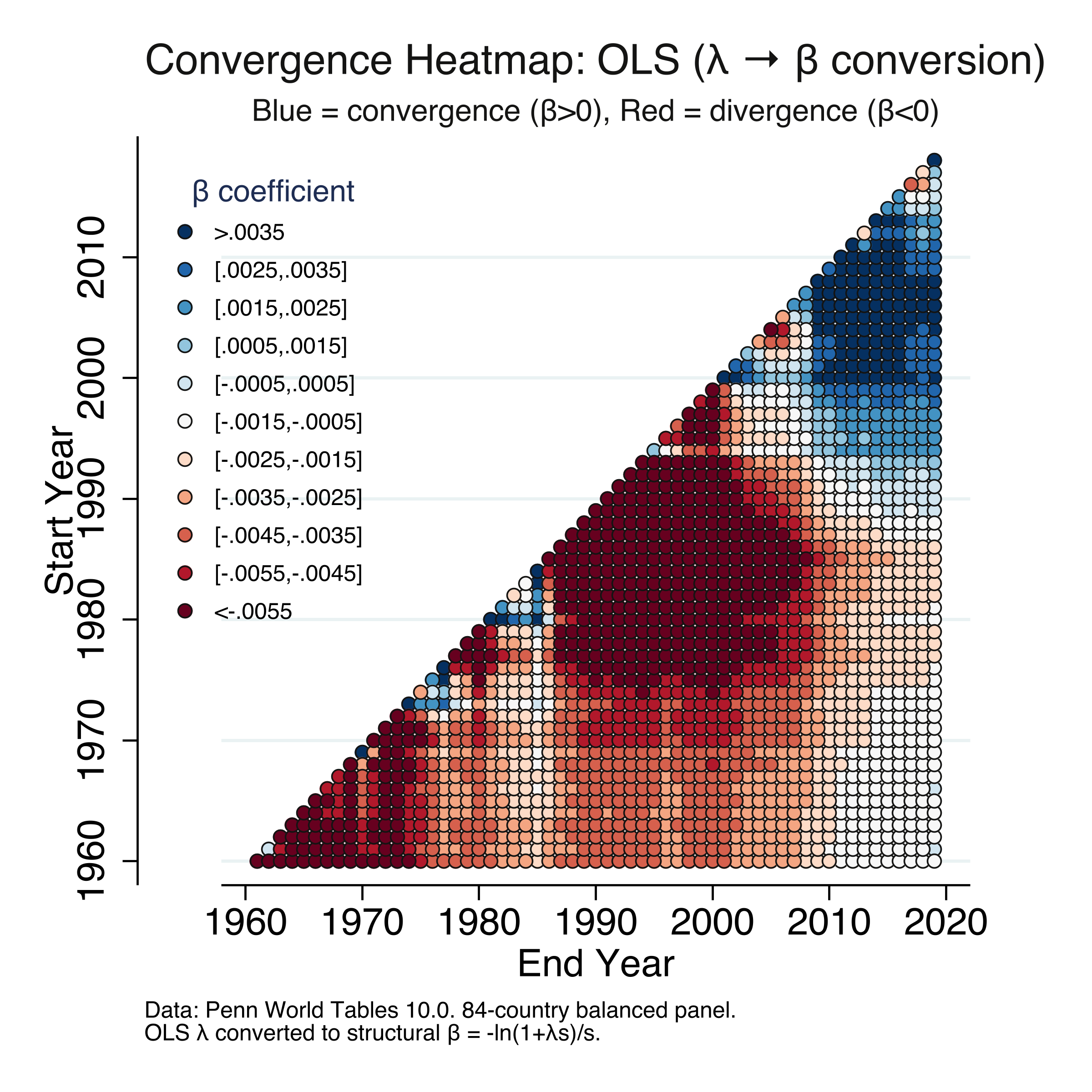

Robust across every window: red divergence before 2000, blue convergence after

Convergence heatmap over all start/end-year pairs (OLS β; the NLS heatmap is virtually identical). Blue = convergence, red = divergence.