Bombs destroy factories — so why do cross-country regressions shrug?

Case studies of individual conflicts paint a dark picture. Yet cross-country regressions of growth on war often return small or insignificant coefficients.

The mismatch is not substantive — it is statistical. Countries that fight wars are not a random subsample of the world. Which countries you compare decides the answer.

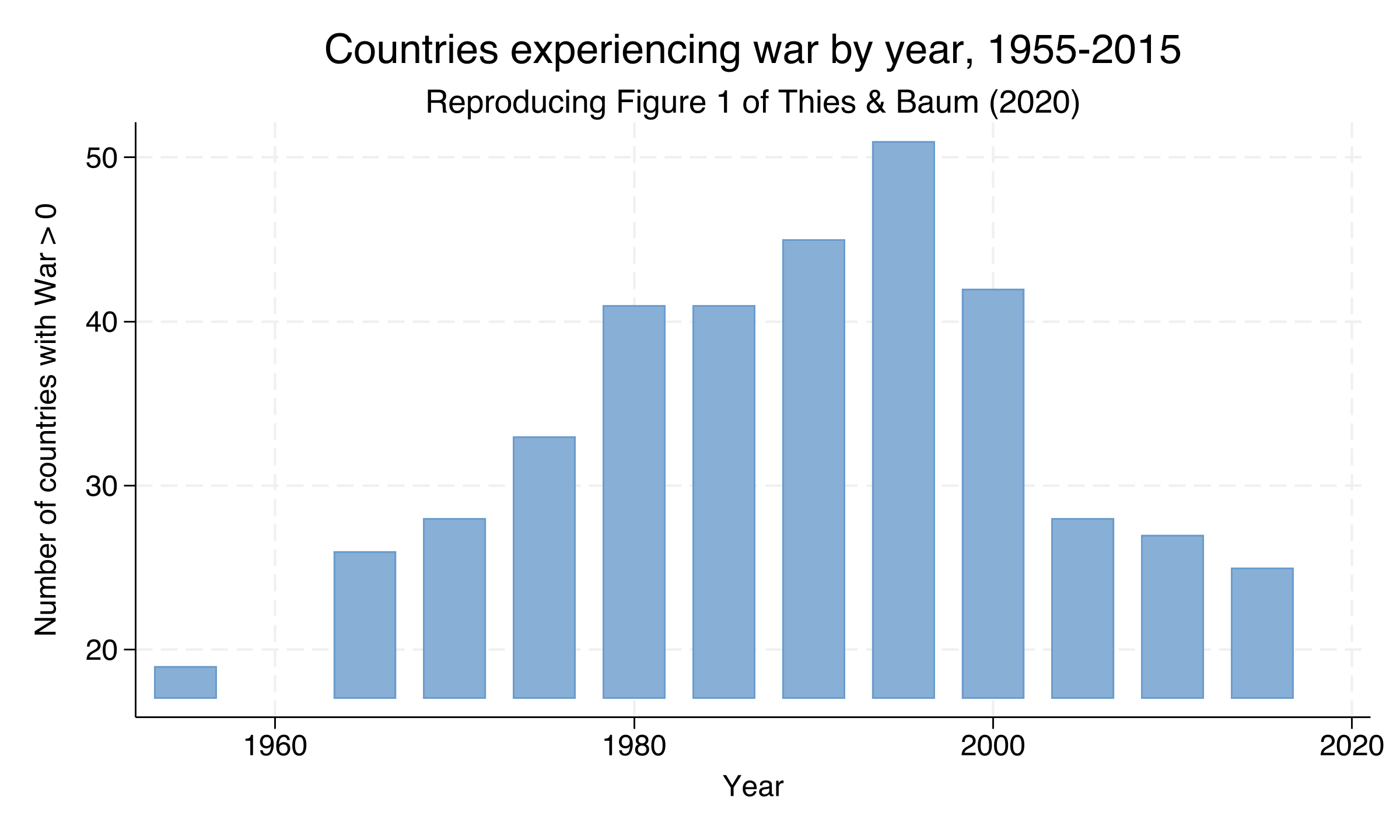

War prevalence peaked at 51 countries in 1990, then plateaued

Number of countries with War > 0 by quinquennium, 1955–2015. Reproduces Figure 1 of Thies & Baum (2020).

Where we’re going

The lab: a 160-country, 1955–2015 panel observed every 5 years

Why static fixed effects fails here — Nickell bias of order \(-1/T\)

Arellano–Bond difference GMM: first-difference, then instrument with deeper lags

Four nested models, the long-run cumulative effect, and AR(2) / Hansen diagnostics

The Investigation

Act II

The lab: 160 countries × 13 quinquennia, 1955–2015

Outcome — \(\ln\) GDP per capita (Maddison, 2011 PPP USD)

Treatment — War intensity, a continuous \(0\)–\(1\) magnitude (\(1\) = Magnitude-7 war)

The lagged term \(\rho\,\ln\text{GDPpc}_{i,t-1}\) captures inertia: income is sticky. \(\alpha_i\) absorbs every time-invariant country trait; \(\delta_t\) absorbs global shocks.

The lag is what makes the model “dynamic” — and what makes it hard to estimate.

Static fixed effects break here — Nickell bias of order \(-1/T\)

Objection. “Just add country fixed effects with xtreg, fe.”

Response. Within-demeaning correlates the demeaned lagged DV with the demeaned error — a mechanical Nickell bias of order \(-1/T\). With \(T \approx 13\) it is too large to ignore, and it propagates from \(\rho\) into \(\beta\).

The fix: first-difference to kill \(\alpha_i\), then instrument the lag

gmm(...) builds the internal lag instruments; iv(...) adds strictly exogenous ones; noleveleq selects Arellano–Bond (difference) over Blundell–Bond (system).

With no controls, a Magnitude-7 war cuts GDP by 0.219 log points

Term

Coef.

SE

\(t\)

Sig.

L.lnGDPpc (\(\rho\))

0.679

0.051

13.21

yes

War (contemp.)

−0.219

0.057

−3.84

yes

Coup (contemp.)

−0.091

0.028

−3.19

yes

N = 1,187 country-years · 155 countries · 146 instruments · AR(2) \(p = 0.091\) · Hansen \(p = 0.184\).

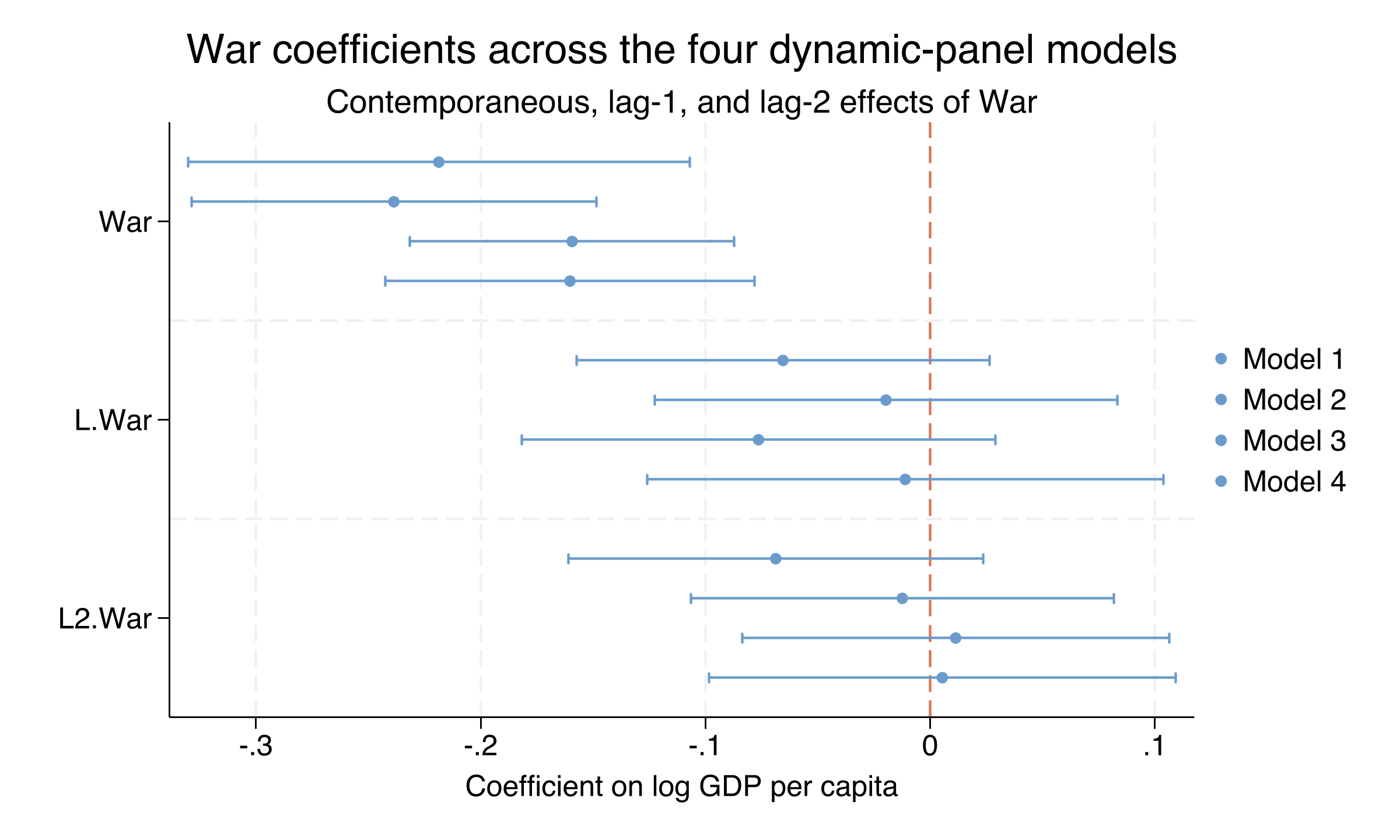

War’s damage is overwhelmingly contemporaneous, not delayed

War, L.War and L2.War coefficients with 95% CIs across all four models. Contemporaneous intervals sit clearly below zero; the lag-1 and lag-2 intervals straddle zero.

The contemporaneous war effect is stable across all four models

Term

(1)

(2)

(3)

(4)

War

−0.219

−0.239

−0.159

−0.160

Coup

−0.091

−0.076

−0.095

−0.090

L.EconFreedom

—

0.020

—

0.028

L.PolitFreedom

—

—

0.0003

0.0002

Economic freedom predicts growth (\(t\) up to 3.31); political freedom never crosses \(t = 1\).

The Resolution

Act III

Over 15 years, a war shock cuts GDP by 0.353 log points — a 30% decline

−0.353

Long-run cumulative War effect, Model 1 (SE 0.079, \(t = -4.48\)) · \(\exp(-0.353)-1 \approx -30\%\)

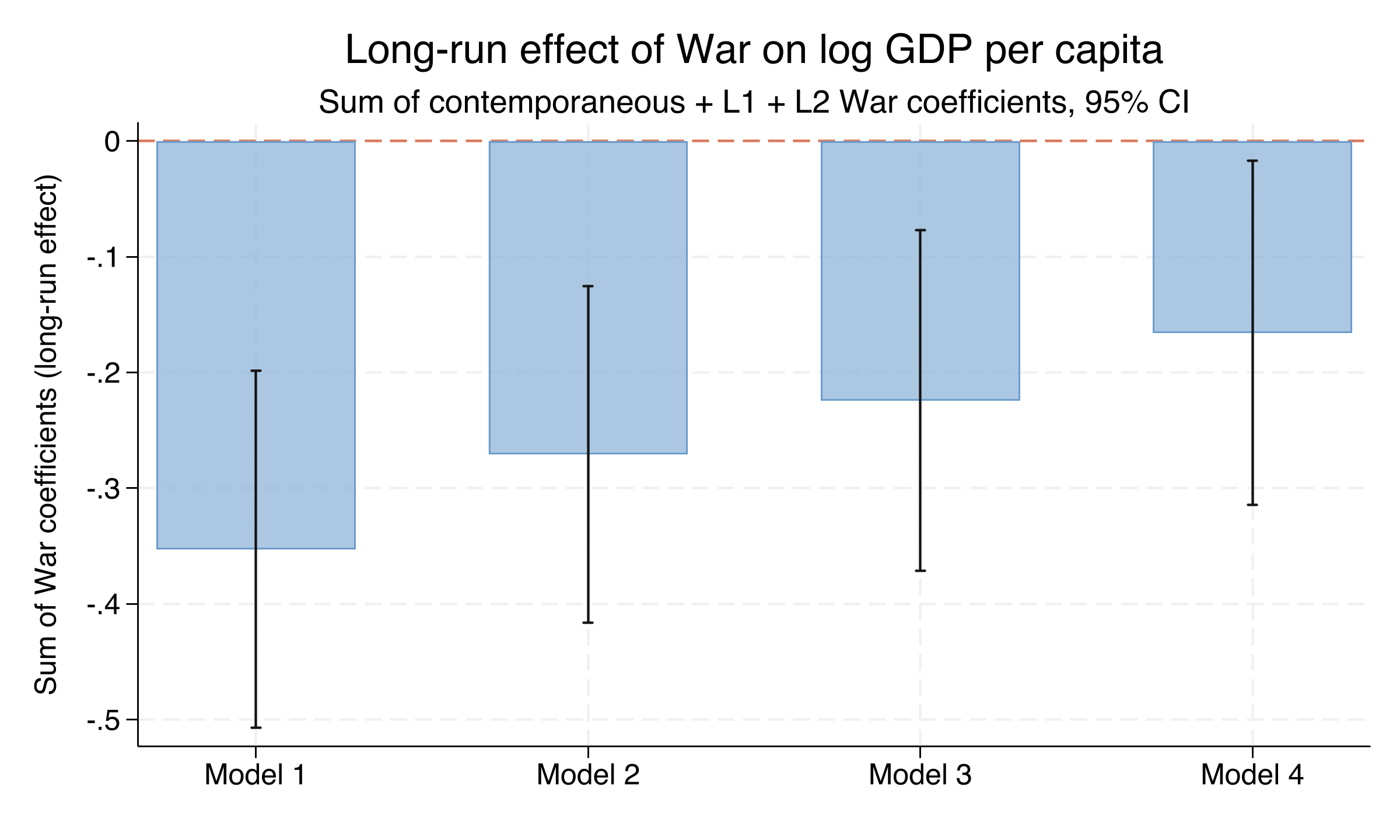

The long-run war penalty shrinks as institutions enter the model

Sum of contemporaneous + L1 + L2 War coefficients with 95% CIs, by model. All bars below zero, shrinking monotonically from −0.353 (Model 1) to −0.166 (Model 4).

Half the long-run war penalty is mediated through institutions

Model

Sum War

SE

\(t\)

Controls

1

−0.353

0.079

−4.48

none

2

−0.271

0.074

−3.65

+ Econ. freedom

3

−0.224

0.075

−2.99

+ Polit. freedom

4

−0.166

0.076

−2.19

+ both

−0.35 → −0.17 is a 53% reduction: war damages institutions, and damaged institutions hurt growth.

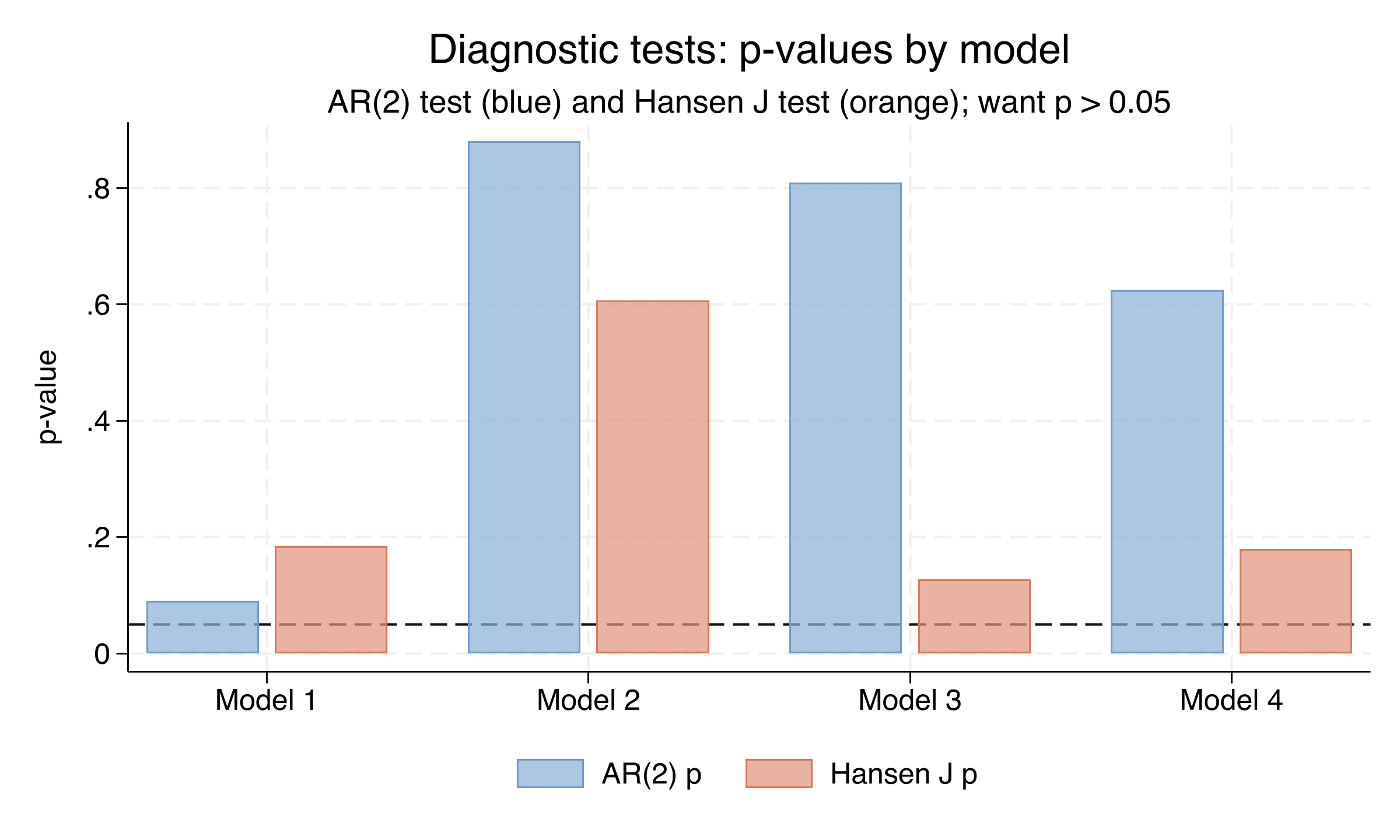

Every model passes AR(2) and Hansen — the strategy is well-diagnosed

AR(2) p-value (blue) and Hansen J p-value (orange) by model, with a 0.05 reference line. All bars above the threshold; Model 1’s AR(2) is closest.

Does GMM make this causal? No — two assumptions still carry the weight

Objection. “Difference GMM with internal instruments recovers the causal effect of war.”

Response. War is a continuous magnitude, not a randomized binary treatment — so this is not an ATE or ATT. The estimate is the within-country dynamic effect, identified only conditional on country and year fixed effects and the dynamic process for GDP. Wars are not randomly assigned.

Let the panel — and the deeper lags — compare each country to itself.